Transformation in Insurance markets post COVID-19

COVID-19 has impacted the insurance industry significantly.

Since the outbreak of coronavirus, there has been a sharp increase in the number of millennials coming forward to enquire and buy comprehensive insurance, i.e. policies covering treatment/ailment that is usually not covered in regular health plans, that covers new diseases. In pre-COVID times the percentage of buyers and intenders for comprehensive plans were 32% and 41% respectively. In the last few months, the demand for such plans saw a significant increase with the percentage of buyers and intenders going up to 55% and 60%.

COVID 19 was the wake-up call for many. The increase in the number of policy takers and intenders among the millennials for comprehensive insurance is a clear sign of rising awareness about such a plan and the importance of having it.

Even before the coronavirus outbreak, the demand for comprehensive coverage was more amongst women than men. Pre-COVID, if 33% of men opted for comprehensive insurance, the demand for the same was 45% among the women, as per the Max Bupa survey.

Now the awareness about comprehensive insurance among men saw a 20% spike with an overall 53% showing interest in the post-COVID times. But in comparison to women, the number is still low. In the last few months, the overall demand for a comprehensive plan among women has increased from 45% to 63%.

Before the pandemic, the biggest concern is people’s minds was increase in personal health/well-being expenses. At least 70% of people thought that way. A common thought that often crossed people’s mind was, considering medical inflation, how will I arrange for money if someone from my family or I fall seriously ill and need to be hospitalized.

But, this thought process has changed significantly since the outbreak of coronavirus. Today, 54% of people are concerned about keeping their family safe from the disease. Meanwhile, 50% of the people are concerned about going out of work or loss of income due to the lockdown. The number of diseases affecting us today are also on the rise. For example, H1N1, Sars virus, Mers virus and most recently COVID -19. Being a pandemic, COVID-19 has left us shaken changing our priorities forever.

First up, we will see a fast-growing trend of innovatively designed health insurance products. In fact, product design has been a key barrier to true digitalization for the longest time. Most insurance providers have been trying to adapt their digital processes to a product that is based on an offline distribution model.

Secondly, we will see a growing acknowledgment of the need to simplify policy documentation. Simplified and uncomplicated policy benefits will need to be accompanied by terminologies and product documentation which are precise as well as easy to understand. This will play a significant role in establishing trust and a truly digital experience; not to mention, a greater access for people across economic and educational backgrounds.

Thirdly, we will see the emergence of a complete digital ecosystem for claims processing and policy management. Be it automated claim adjudication that can significantly improve decision-making times, or better digital controls at the provider and insurer’s end, customers are looking to significantly faster claim settlements which require minimal manual processing.

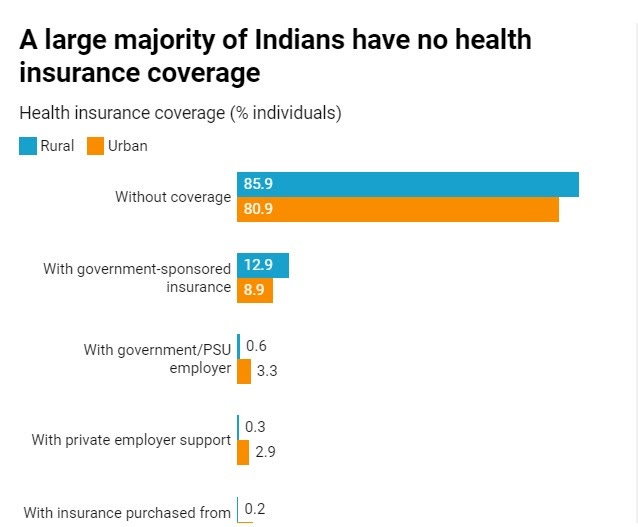

As of 13 November, PM-JAY had issued 126 million e-cards to individuals. Even if one assumes all these 126 million individuals did not have any health cover previously, that still leaves about 1 billion Indians uninsured. While PM-JAY is a step in the right direction, its selection criteria is stringent, based on data from the Socio-Economic Caste Census (2011), restricting eligibility.