Bancassurance ! Its time to go digital. Reigniting Bancassurance

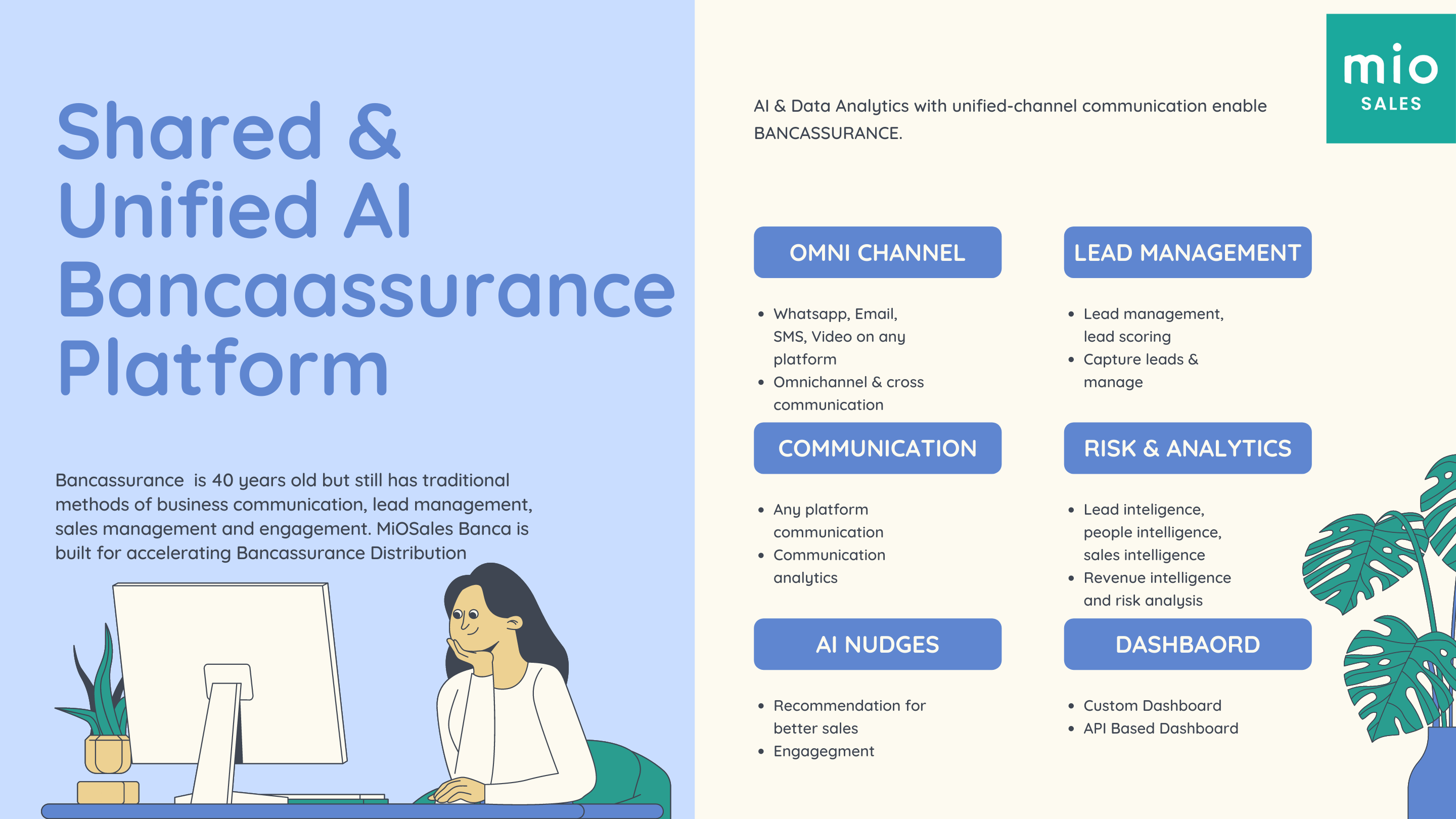

MioSales Banca is AI sales platform for financial institutions, distributor, banks and brokers for enabling next-gen sales, lead, marketing & engagement

An accelerated pace of digitalization in the financial sector across the Asia-Pacific (APAC) region due to the COVID-19 pandemic is expected to support the growth of online life bancassurance, according to GlobalData, a leading data and analytics company.

GlobalData’s latest report, ‘Global Bancassurance Market to 2025 – Analysing Key Performance Indicators, Key Trends, Drivers and Challenges, and Competitive Landscape’, reveals that in APAC, prolonged period of low interest rates aggravated by lackluster credit growth due to the pandemic highlighted the need for banks to diversify their revenue options.

As a result, banks and insurers are leveraging technologies such as artificial intelligence, robotic process automation, open finance and blockchain to understand customers preference and provide personalized solutions in real-time.

Bancassurance has been around for about 40 years, providing an effective channel for selling insurance products through banks. However, clients have now mostly switched to digital services. Banking and insurance organizations thus need to respond to the change and enhance their offerings. The customer need for a digitalized experience will only be heightened, which is why digitalisation in bancassurance gains importance.

Refining your partnership is key to ensuring you can adequately meet client demands. In this entry, we’ll explain why bancassurance companies are better off with a digital approach and provide key tips on implementing it.

Why is the switch to digitalization highly recommended?

Transitioning from reliance on face-to-face interactions to digital services is practically inevitable. Banks and insurance companies that have completed the transition are seeing significant rates of growth.

According to a study by McKinsey & Company, digitization has driven development in many bancassurance organizations. Businesses that have digitalized non-life product sales have seen a growth of nearly 20%.

On the other side of the aisle, institutions that haven’t moved their operations to the digital realm have experienced stagnating rates. This means that customers appreciate and expect a digital bancassurance experience, not an outdated model.

That said, companies have seen many obstacles on their way toward digitalization. Competing banking products and intricate sales processes are some of the main culprits.

Nevertheless, the potential for growth with digital bancassurance sales is too great to be missed. More than three out of four Americans prefer a digitalized portfolio, providing a large customer base where you can sell your products. All you need is the right strategy, and you’re about to find out what it looks like.

As customers and banks shift to digital technologies, bancassurers need to rethink their distribution model.

As a distribution channel for a wide variety of insurance products, bancassurance has seen surges and stalls over the past several years. In the second quarter of 2018, McKinsey hosted its annual global Bancassurance Forum in Rome where it presented new research and data from a comprehensive benchmarking study by Finalta,1 covering banks headquartered in 27 countries.2 Overall, the bancassurance industry has seen strong premium growth around the world. From 2011 to 2017, the growth of the bancassurance channel outpaced other channels in both life and non-life products (exhibit). In the past two years, however, growth seems to be slowing in non-life.

The findings also highlight digitization as a core ingredient of growth. Our assessment identified a cadre of European “growth champions” that achieve annual digital sales of non-life products at twice the average of their European peers. From 2016 to 2017, when much of Europe experienced stagnating growth, new business sales by these growth champions grew 17 percent. In other words, customers have taken notice—and many have now come to expect the kind of bancassurance experience that only digital products can provide.

Banks have been slow to move their bancassurance products down the path toward digitization, however. Complex sales processes for insurance products, as well as competing priorities with other banking products, may be to blame. Still, in the face of record-low interest rates, many banks see the potential non-interest income that bancassurance can offer and have been seriously considering their bancassurance strategies. Enabled by digital processes and analytics, three essential components—personalization, superior customer experience, and omnichannel engagement— will shape the winning formula for sustained bancassurance growth.

The current state of bancassurance

Banks in many markets—particularly Asia–Pacific and Latin America—have been clearly focused on the bancassurance channel for selling life insurance products, which tend to have higher average sale prices and profit margins than most non-life products. Indeed, life products fit particularly well into the bancassurance framework. They are related to financial products—credit life products skyrocketed with the credit boom of the 2000s, for example. And where banks have access to their clients’ personal financial assets, they often work to promote life policies with built-in cash value as an alternative form of investment, citing tax benefits.

In contrast, many banks have been deterred from putting much effort into marketing non-life insurance products, which have lower average sale prices and commissions. Few banks have meaningfully increased sales penetration of auto and commercial lines, though many banks have done reasonably well coupling home insurance with mortgage products. More recently, banks—reacting to historically-low interest rates—have been on the hunt for new sources of non-interest income. And as a result, they have started to recognize the potential of stand-alone non-life product sales.

Overall, global bancassurance sales grew across all regions from 2011 to 2017, led by Latin America, where premiums expanded 12 percent. Asia–Pacific’s sales grew by 9.2 percent, with China accounting for two-thirds of the growth. In both regions, the growth can be explained by banks’ motivation to increase revenues in the face of shrinking net interest margins. Also, the rapid increase in per-capita GDP and living standards across much of Latin America in the 2000s led to more disposable income, and more people buying insurance products in general. In terms of penetration, the Asia–Pacific market is bifurcated: on one hand, bancassurance now accounts for 30 percent of total new life insurance business. On the other hand, bancassurance as a share of the banks’ total customer base remains at a low level, often ranging from 1 to 4 percent. Relatively low European penetration rates of 37 percent in life and 8 percent in non-life products suggest that there is plenty of room for bancassurance sales to grow. Whether banks are looking to increase sales of non-life or life products, the use of digital tools will be key. Whether banks are looking to increase sales of non-life or life products, the use of digital tools will be key.

Banks have been slow to sell bancassurance digitally

Finalta’s survey of 118 banks around the world found digital bancassurance channels accounted for 19 percent of bancassurance non-life sales (up from 12 percent in 2015). Meanwhile, digital bancassurance channels accounted for only 2 percent of life sales, where branches and physical advisers remain dominant (85 percent of sales in 2017).3 This disparity may exist simply because, with rare exceptions, banks do not offer these products digitally. Banks, have been slow to digitize because complex sales processes for insurance can make the move to digital channels more challenging. Finally, some banks might not see life insurance as a priority investment solution given increasing regulatory contracts (such as MiFID II) and the dilution of tax benefits in some markets.

While every bank follows its own path toward creating a winning multichannel model, few have mastered the game and excel digitally. Most banks continually evolve their digital strategies and review the “core” of their digital offer. In this process, however, banks often treat bancassurance products in a tactical, rather than a strategic way. As a result, banks tend to insert these products into other offerings rather than making them a discrete part of their digital channel strategy.

In short, fewer customers visit physical bank locations, and banks have been slow to make up for lost branch sales by implementing a comprehensive digital model for bancassurance. The lack of such a model becomes even more relevant when considering many banks’ renewed focus on lending products sales. The combination of fewer visits and an increased emphasis on lending products diminishes opportunities for selling non-lending products—such as bancassurance. Therefore, it is pivotal that banks find smart ways to sell bancassurance digitally. Source

It is important to drive the future value of Bancassurance. New Age Bancassurance needs:

Winning with digital and analytics in bancassurance

Personalization that makes the most of unique banking data and analytics

The data make it clear that digitization is a core ingredient of growth.

Superior, digitally enabled customer experience

Bancassurers need simple, fully automated, and end-to-end processes that reduce barriers to sales in digital channels.

Omnichannel customer engagement

MiOSales Platform designed for Bancassurance for future allowing sales team to have better experience, building partnerships & relationships, increase in customer base, Improvement in ROI and get better insights, recommendation & analytics.

Lets reignite Bancassurance together. Please wrtie to contact@artivatic.ai or hello@miosales.com

MiOSales Website: www.miosales.com

Artivatic Company Website: www.artivatic.ai